We collaborate to achieve sustainable success

A leading environmental solution provider

Get in touch with usAFS Energy EU ETS Market Report - Week 14 2026

Do you want to receive to-the-minute up to date info? Please sign up to our client portal and/or to the Viridian Exchange.

Previous Week Events:

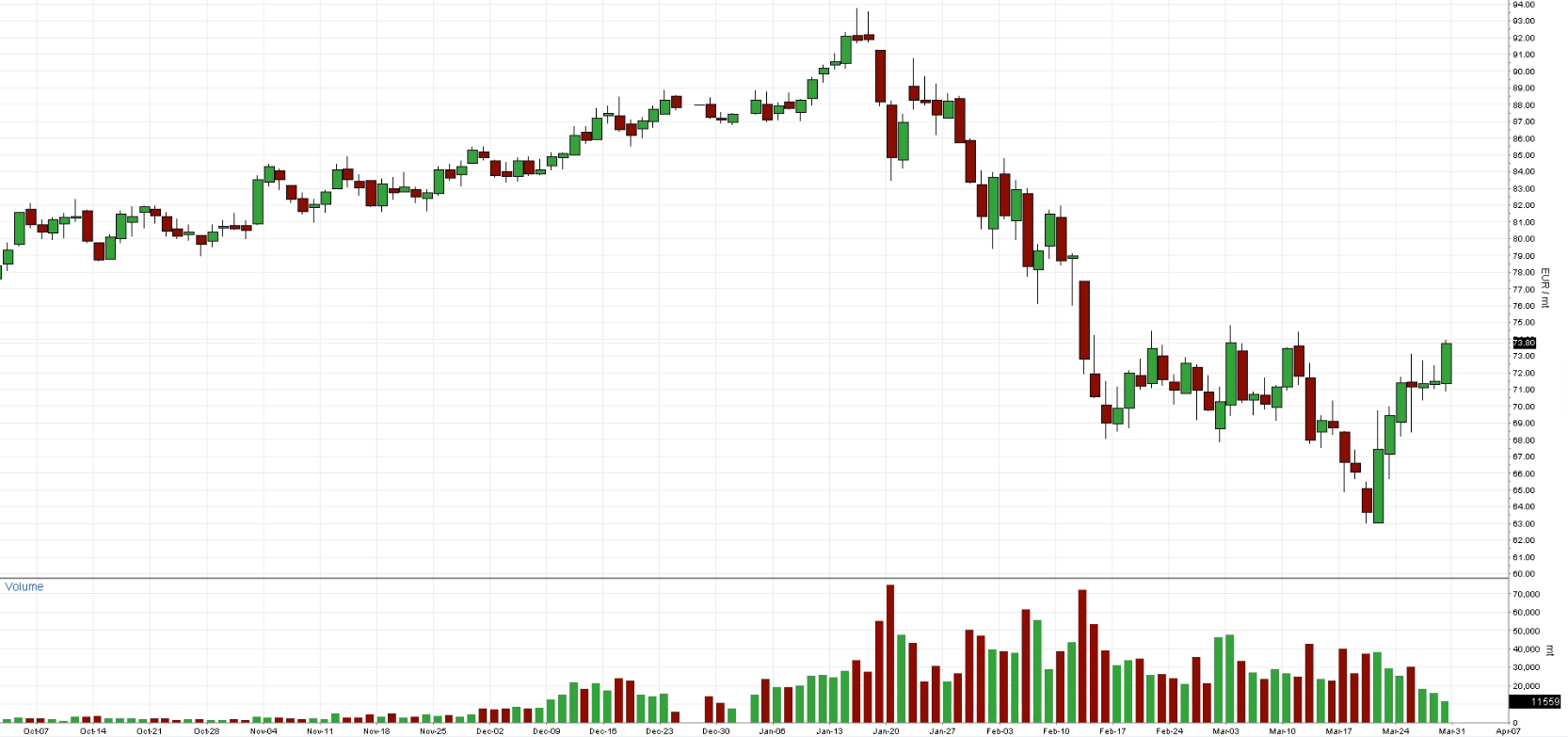

Last week, EUAs declined 6.18% from Monday’s open (65.87) to Friday’s close (69.94); weekly high (71.50) / low (64.45) spread was €7.05

Auction volume: 9.23 million EUAs, same as last week.

Energy Fundamentals

The fundamental backdrop remains highly supportive for energy prices, with European gas storage falling further to 28.1% as of March 28, 2026. Inventories remain low for this stage of the year, while the ongoing conflict involving Iran continues to increase concerns around future supply availability. The longer the crisis persists, the greater the risk that Europe enters the next injection season without being able to sufficiently rebuild inventories ahead of winter. Geopolitical developments continue to dominate sentiment. Oil has moved above $115 per barrel as the Iran conflict entered its fifth week, reflecting fears around disruptions to flows through the Strait of Hormuz. At the same time, reports that Iran is allowing Spanish vessels to transit the strait suggest that flows are not completely shut off, although access appears increasingly politicized. Trump’s comments regarding potentially “taking the oil in Iran” and his willingness to tolerate certain Russian oil shipments also reinforce the perception that energy markets are becoming more politically driven and unpredictable. High energy prices are already beginning to affect fuel-switching behavior. The gas supply shock is reportedly pushing some of the world’s largest energy consumers back toward coal usage, highlighting the strain elevated gas prices are placing on utilities and industrial demand. This may temporarily soften gas consumption in some regions, but it also underscores the difficulty of balancing affordability, security of supply, and decarbonization goals. On the policy side, attention remains focused on the EU ETS. Reform proposals around the supply reserve and free allocation benchmarks are expected to be confirmed on April 1, while comments from some EU officials suggest that there is limited appetite for a more radical overhaul of the system. This points toward targeted adjustments rather than broad structural changes. For investors, the current environment remains shaped by a tension between short-term energy security concerns and the longer-term push toward climate neutrality, keeping both energy and carbon markets highly volatile.

- Gas storage currently sits at 28.1% (March 28th, 2026)

- Iran War’s Gas Supply Shock Pushes Top Consumers Back to Coal

- Donald Trump says US could ‘take the oil in Iran’

- Iran reportedly allows Spanish ships to transit Hormuz strait due to position on war

- Oil rises above $115 and Asia shares slide as Iran war enters fifth week

- Trump says he has ‘no problem’ with Russian oil tanker bringing relief to Cuba despite blockade

- Reform proposals of EU ETS supply reserve and free allocation benchmarks confirmed for Apr. 1

- Estonian minister: No need for more thorough Emissions Trading System changes

- The transition to climate neutrality can go hand-in-hand with sustainable public finances

- What the EU ETS upheaval means for investors

Investment Funds

- Investment funds decreased their net long position to +32.77m EUAs on March 13th (vs. +39.01 EUAs on March 13th).

- Gross short positions increased to -48.67 EUAs (vs -47.84m EUAs).

- Gross long positions decreased to 81.44 mln EUAs (vs. 86.84m EUAs).

Market Prices

- Indicative Dec26 EUA Price: €72.09

- Indicative Spot EUA Price: €71.49

- YTD Spot EUA Price: € 71.18

- MTD Spot EUA Price: € 68.43

Chart A: December 2026 EUA Price (EUR)

Technical Analysis

Dec 26 price action has improved noticeably after rebounding from the recent lows near €63–64. The market has now pushed back above the short-term moving averages and is trading around the €73 area, which marks an important recovery zone after the sharp sell-off seen earlier in the quarter. The sequence of lower highs has not yet been fully broken, but the recent structure suggests that bearish momentum is fading and that a broader stabilization phase is developing. The Bollinger Bands have started to tighten after the earlier expansion to the downside, providing an indication of cooling volatility. Price has moved back toward the upper half of the range and is now approaching the mid-band resistance area near €74–75. A sustained break above this zone would strengthen the short-term outlook and could open the door toward the 50-day moving average near €71 and potentially higher levels beyond that. The 20-day MA has flattened and price is now trading above it, while the 50-day and 100-day MAs remain above current levels and continue to act as overhead resistance. This keeps the broader structure cautious, but the recent move higher suggests the market is attempting to build a base after the extended decline. Momentum indicators are turning more supportive. RSI has recovered toward the mid-50s, suggesting improving strength without yet being overbought. CCI has moved back into positive territory, reflecting stronger short-term momentum, while MACD remains negative but continues to rise steadily, indicating that downside momentum is fading.

The short-term tone has improved following the rebound from the lows, with price now testing an important resistance zone around €73–75. A sustained break above this region would strengthen the recovery outlook and could trigger a move toward higher resistance levels. If price fails to break through, the market may remain stuck in a broader consolidation range, though the immediate downside pressure appears to have eased significantly.

Chart B: December 2026 EUA Price (EUR) - Technical

AFS ENERGY B.V.

The information contained in the AFS Energy EU ETS Report, hereinafter Report, has been compiled or arrived from sources believed to be reliable but no representation or warranty, express or implied, is made as to their accuracy, completeness, timeliness, correct sequencing or correctness.

AFS Energy B.V. does not accept any liability, contingent otherwise for (i) the accuracy, completeness, timeliness or correctness of any information provided in the Report, (ii) any decision made, or action taken by you in reliance upon any of them and (iii) any direct or consequential loss arising from the use of the Report. AFS Energy B.V. does not make any representation or warranty about the suitability of the information in the Report.

The information contained in the Report is published for the assistance of the recipient but is not to be relied upon as authoritative or taken in substitution for the exercise of judgement by any recipient.