We collaborate to achieve sustainable success

A leading environmental solution provider

Get in touch with usCBAM Status: Certainties, Gaps & Next Steps

The EU’s Carbon Border Adjustment Mechanism (CBAM) has reached another key milestone. The long-awaited CBAM Omnibus Regulation has officially been published in the EU Journal, marking the completion of the legislative process. While this provides much-needed legal certainty confirming that CBAM will move forward as planned in January 2026, several crucial elements for the definitive CBAM period remain undefined, leaving importers in a state of uncertainty about their future obligations and financial exposure.

Key Updates from the Final CBAM Text

The CBAM Omnibus introduces several important changes from the original proposal, including:

- Compliance threshold set at 50 tonnes/year of CBAM goods.

- CBAM declaration deadline moved to 30 September.

- A quarterly minimum of 50% of required certificates must now be held.

- The sale of CBAM certificates will begin in February 2027, applying retrospectively to 2026 imports.

- Certificate pricing:

- For 2026 imports, the CBAM certificate price will be based on the quarterly average EUA price in 2026 of the quarter corresponding to the import.

- For 2027 onwards, the price will shift to a weekly EUA average.

- For 2026 imports, the CBAM certificate price will be based on the quarterly average EUA price in 2026 of the quarter corresponding to the import.

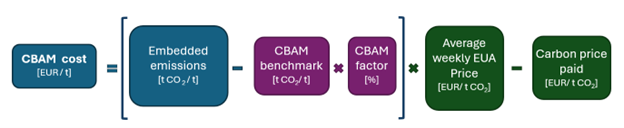

Estimating CBAM Financial Exposure: variables check

For importers, understanding CBAM’s financial impact is essential. However, many variables in the CBAM cost formula (see below) remain unsettled. Below, we unpack the formula and discuss each variable individually to review where CBAM developments actually stand.

1. Embedded Emissions

Embedded emissions in the definitive CBAM period can be determined using either actual or default values.

Actual Values

During the transitional period, importers were expected to collect emission data from their suppliers to prepare for the shift to the definitive phase. These “actual” values should now form the foundation for compliance reporting. However, as confirmed by several market participants, most authorised CBAM declarants continue to struggle to obtain accurate and complete emission data from suppliers.

Moreover, the collected data will need to undergo official verification before submission of CBAM reports. This verification process is scheduled to start in 2027, meaning that the accuracy and reliability of current CBAM cost estimates remain uncertain until these verifications are completed.

Default Values

If supplier data is unavailable, unattainable, or deemed unreliable, importers may rely on default values. However, several critical aspects remain unresolved:

- Definitive-period default values have not yet been published.

- The EU methodology for calculating these values will change. Instead of using the average of high-emitting EU producers (as was done during the transitional period), the new default values will reflect the worst-performing producers per country of origin.

- For products with multiple production routes, the most emission-intensive process will be assumed.

- The European Commission is also expected to apply an additional markup.

Taken together, these adjustments will make default values more conservative than those used during the transitional period, a clear signal that importers are being encouraged to obtain verified actual data directly from their suppliers.

A draft of default values is rumored for release by the end of October, marking a significant milestone for importers seeking to refine their CBAM cost forecasts ahead of the definitive period.

2. CBAM Benchmarks

CBAM benchmarks, essential reference points for calculating liabilities, have not yet been published. The Commission has announced a delay, pushing their release to Q1 2026, following the revision of EU ETS benchmarks, however, a provisional version may appear toward late 2025.

Key expectations:

- Benchmarks will differ from EU ETS values as CBAM operates at the product level rather than installation level.

- They could distinguish between default and actual benchmarks or use aggregated values, though these remain speculation and the methodology chosen by the European Commission to determine these crucial values remains unclear.

In summary, although not clarified officially yet, it is to be expected that benchmark values will be more complex than just a fixed value per CN code.

3. CBAM factor

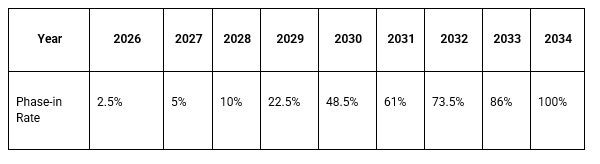

One area where clarity finally exists is the phase-in of CBAM and the phase-out of free allowances under the EU ETS. The timeline has been clear and consistent since the original CBAM Regulation was published in 2023, and it remains unchanged in the recently adopted Omnibus text. Starting in 2026, 2.5% of free allowances will be replaced by the CBAM levy, with a full transition by 2034, as illustrated in the table below.

4. EUA Price

The EUA price, central to CBAM certificate price, is a known variable, yet one that remains exceptionally difficult to forecast with confidence. Its value is inherently dynamic and volatile, shaped by the interplay of multiple overlapping EU climate policies and evolving market conditions. What is clear, however, is that the EU ETS cap will continue to tighten while demand for allowances remains robust, creating sustained upward pressure on carbon prices in the coming years.

Most carbon market analysts anticipate a gradual but steady increase in EUA prices, suggesting that importers should prepare for higher CBAM compliance costs through 2030 and beyond.

5. Carbon Price Paid

Another key variable, the carbon price paid in the country of origin, remains without an implementing act which will be fundamental in clarifying how this potential discount will be applied. The European Commission is expected, by end of 2025, to publish a list of recognized carbon pricing systems outside the EU. This will clarify how importers can claim credits or discounts based on carbon prices already paid abroad. Until then, uncertainty persists regarding how foreign carbon costs will be verified and deducted from CBAM obligations.

Looking Ahead: Practical steps & AFS Energy offering

The official publication of the CBAM Omnibus Regulation marks a major step toward full implementation, but many practical details remain unresolved.

For importers, the focus should now be on:

- Strengthen supplier data collection and ensure traceability throughout the value chain.

- Monitor upcoming implementing acts that will clarify crucial details such as default values, benchmark methodologies, and carbon price recognition.

- Design a robust CBAM risk management strategy, integrating data, pricing, and procurement considerations.

CBAM compliance will soon become a defining element of trade with the EU, and the coming months will be critical for companies preparing to navigate the definitive CBAM period with confidence and clarity.

It is essential to keep in mind that purchasing decisions made today can directly affect your CBAM exposure for 2026. Goods ordered now may arrive at the EU border in early 2026, meaning they will fall under CBAM obligations. Even if the financial impact is not immediate, CBAM costs are already accumulating in the background.

Therefore, act now to gather data from your suppliers. Use trusted platforms to simplify and streamline data collection and to obtain a reliable estimate of your CBAM exposure.

Once you have assessed your exposure, the next step is to actively manage it. EU Allowances (EUAs) represent the natural hedging instrument against CBAM costs. AFS Energy offers the first platform in Europe designed to help companies seamlessly purchase EUAs and manage their CBAM-related carbon exposure effectively.

Get in contact with our team to discuss your CBAM objectives, discuss procurement strategies and get access to our trading platform.